Founded in 2014, Ninja Van is one of leading logistics companies focusing on last-mile delivery across Southeast Asia including Singapore, Malaysia, Vietnam, Indonesia, Philippines, and Thailand. I visited Ninja Van’s fulfillment centers and warehouses in Malaysia in 2019, and the efficiency of sorting, high distribution area coverage and technology orientation impressed me a lot. According to ACRA, Ninja Van’s momentum kept going since then, with revenue growing at a compound annual growth rate (CAGR) of 110% from 2019 to 2021, implying a doubling every year.

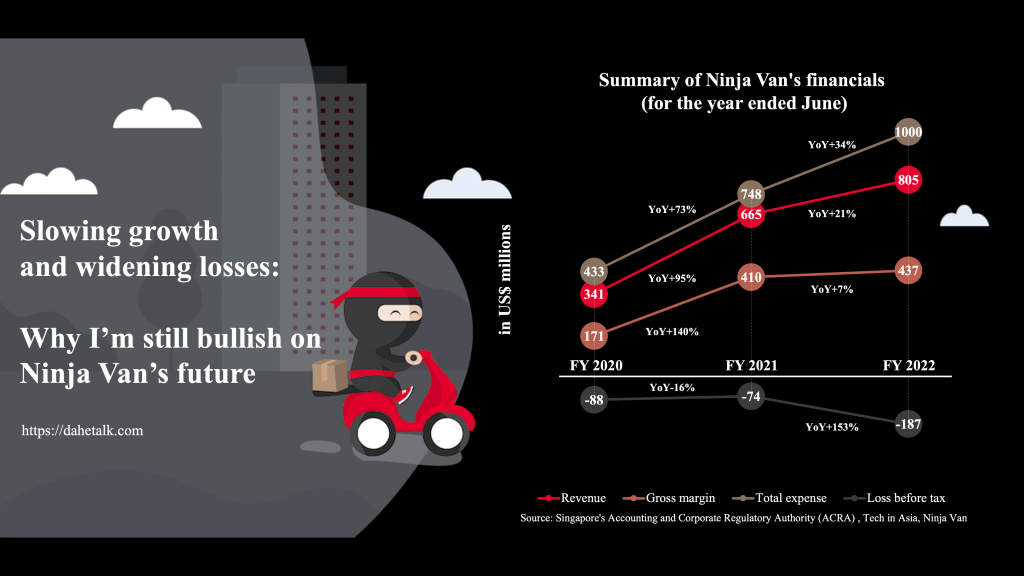

However, Ninja Van has revealed its latest financial status recently. Revenue year-on-year (YoY) growth for FY 2022 decreased markedly from 2021’s 95% to 21%. The gross margin declined from 62% to 54% and the expense YoY growth went up to 34%. To sum up, growth in expense is outpacing growth in revenue, resulting in widening losses.

Essentially, why did that happen? It can be attributed to three main issues.

First, in terms of the slowing revenue growth, the pandemic has been boosting ecommerce development in the last 2-3 years, leading the delivery volumes to surge, but the bonuses are getting to taper off now. The high base period last year caused the revenue growth rate to go down this year.

Second, in terms of decreasing gross margin, as ecommerce majors like Shopee are seeking for higher profit, they are trying to squeeze logistic costs from third-party logistics (3PL) firms, and even gradually reducing the reliance on 3PL firms, building their own in-house logistic teams like Shopee Xpress. For example, Shopee Philippines cut the cord with Ninja Van a few months ago. What’s more, Grab and GoTo have begun offering instant and same-day delivery services in Indonesia.

Third, in terms of higher expense rate, the founder of Ninja Van attributed that to the investment on automated parcel sorting systems across its nine regional hubs in Southeast Asia since 2021, and it is expected to be completed in 2H24.

In my view, the first issue is short-term and could be ignored, and the momentum of the growth will carry on. Though the ecommerce bonuses due to the pandemic are disappearing, the online shopping behavior is still diffusing. In addition, according to the report from Research and Markets, the e-commerce logistics market in southeast Asia is poised to grow by $58.93 billion during 2022-2026, accelerating at a CAGR of 20.16% during the forecast period. The market size is big enough and we can still see a double-digit growth rate in the next few years.

On the other hand, the second and third issues are highly related. While ecommerce platform heavyweights operate their own in-house delivery fleets, they are unlikely to ditch 3PL firms entirely. For instance, in-house fleets may not be able to offer service in specific areas or afford the delivery volumes during peak periods. Having 3PL firms like Ninja Van makes ecommerce platforms more flexible without heavy investment.

Facing the intensifying competition from peers, new entrants and in-house fleets, the critical tactics for Ninja Van is not only to expand other revenue streams, like increase the turnover proportion of small and medium-sized e-commerce sellers or independent shippers, but also concentrate on enhancing the delivery efficiency via optimized algorithms and better sorting facilities.

A lot of competitors in the logistics industry were unable to find an obvious differentiator, so they differentiate on price. However, they may suffer significant losses before they find the way to drive the cost down. Once they burned out the cash, they were squeezed out from the market, so that’s an unsustainable business model.

In essence, the logistics industry values economics of scale and process efficiency above everything else. That is the reason why Ninja Van keeps investing a lot in infrastructure and technology, making the logistic network much denser and more efficient, leading to lower cost, and attracting more clients lastly.

Accordingly, though the expense of Ninja Van spiked, it is an inevitable journey to build the moat in the logistics industry. In the light of whole market potential and strengthening moats, Ninja Van is expected to maintain its position as an industry leader though it is highly likely that the losses may persist or worsen through 2023-2024.

Luckily, thanks to the Series E fundraising in September 2021 from investors including Alibaba, Monk’s Hill Ventures and B Capital, Ninja Van’s cash on hand amounts to US$449 million. Considering the operating outflow of US$122 million in FY 2022, implying a runway of over 3.5 years, the cash cushion provides Ninja Van great resilience in the fierce competition.

.

成長減緩、虧損擴大:為什麼我仍然看好Ninja Van的未來?

成立於2014年的Ninja Van是東南亞物流界的獨角獸公司,在新加坡、馬來西亞、越南、印尼、菲律賓及泰國等國深耕最後一哩路的配送服務(last-mile delivery)。

我曾在2019年時拜訪了Ninja Van在馬來西亞的配送倉儲中心,它們高效的分揀速度、大面積的配送範圍、以及技術驅動的成長軌跡,讓我印象相當深刻。根據ACRA的數據,Ninja Van從那時就一直保持增長,自2019到2021年的營收年複合增長率(CAGR)高達110%,代表每年翻了一倍。

然而,Ninja Van最近公布了其最新的財務狀況。2022年的營收年增長率(YoY)從2021年的95%下滑至21%,毛利率從62%下降到54%,而營業費用年增長率也來到了34%。當營業費用的增速大於營收的增速時,就導致了虧損加劇。

.

成長減緩、虧損擴大,背後的原因是什麼呢?

首先,就「營收增速趨緩」來說,由於過去兩三年的疫情加速了電商的發展,導致物流需求激增,但現在這種增長已逐步放緩,因此去年墊高的基期,必然造成今年營收增速的下降。

其次,就「毛利率下降」而言,像Shopee這樣的電商巨頭們,為了提升獲利,持續從第三方物流公司(third-party logistics ; 3PL)中壓縮物流成本,甚至開始減少對3PL公司的依賴,建立自己的內部物流團隊,像是Shopee Xpress。舉例來說,菲律賓的Shopee在幾個月前就與Ninja Van停止合作。而像Grab和GoTo這樣的超級app,也開始提供即時配送服務,更為整個產業帶來更高強度的競爭。

第三,在「費用增速提升」方面,Ninja Van將其歸因於自2021年以來在東南亞九個區域中心所投資的自動包裹分揀系統,預計將於2024年下半年完成,因此未來幾季的財報還會慢慢反應這些費用。

在我看來,第一個問題應該是短期現象,儘管因疫情而產生的電商紅利正在消失,但整個東南亞的網購行為仍在普及中,長期看來增長的動能仍然會持續下去。此外,根據Research and Markets的報告,2022年至2026年東南亞電商物流市場有望增長589.3億美元,年複合增長率為20.16%,因此在市場規模夠大,未來幾年仍有兩位數增長的情況下,相信Ninja Van還是能從大環境中獲得ㄧ定的成長動能。

而在毛利下滑和費用增長方面,我認為兩者是高度相關的。雖然電商平台巨頭紛紛建立自己的物流團隊,但它們其實也不大可能完全不與第三方物流(3PL)公司合作。例如,它們自建的物流車隊可能沒法觸及所有區域,或是在運力高峰期承擔高運輸量。跟像Ninja Van這樣的第三方物流公司合作,可以讓電商平台的調度更具靈活性,也不需要進行巨額投資。

面對日益激烈的競爭,Ninja Van的關鍵策略除了要擴大其他收入來源(例如:增加中小型電商平台、獨立賣家的營收比重)外,更要透過演算法優化和更好的分揀設施來提高配送效率。

在物流行業,多數廠商很難做到差異化,因此競爭的手段往往淪為價格戰。然而,在價格降低、成本不變的情況下,也會讓它們遭受更多的虧損。一旦他們燒完了資金,就只好離開市場。

.

回歸物流業的本質

從根本來看,其實物流業最看重就是「規模經濟」和「流程效率」,這也是Ninja Van不斷投資基礎設施和相關技術的原因,目的是讓物流網絡變得更加龐大及高效,進而降低成本、吸引更多客戶。因此,儘管短期看來Ninja Van的支出持續飆升,但長期看來,這是在物流業建立護城河所不可避免的過程。

總的來說,有鑒於東南亞物流市場的整體潛力、以及Ninja Van在強化護城河上的努力,我認為Ninja Van將保持其在行業領導者的地位。雖然短期看來,它的虧損可能會持續,甚至在2023-2024年加劇。

幸運的是,Ninja Van在2021年9月時,從阿里巴巴、Monk’s Hill Ventures和B Capital等投資者募得E輪融資,目前Ninja Van手上現金仍有4.49億美元,若以2022年其的營業現金流出1.22億美元來看,意味著Ninja Van尚有超過3.5年的Run way,能讓它在激烈的競爭中保有更多的底氣。

感謝分享!

讚讚